25. Tax credit for children's activities (Line 462)

You can claim a refundable tax credit for a child's physical activities (This link will open a new window) or artistic or cultural activities (This link will open a new window), provided you meet all of the following conditions:- You were resident in Québec on December 31, 2013.

- In 2013, you or your spouse on December 31, 2013 (This link will open a new window), paid to either

- register an eligible child (This link will open a new window) in a recognized program of activities (This link will open a new window) (physical activities or artistic or cultural activities) offered in 2013 or in a subsequent year; or

- obtain a membership for an eligible child in a club, association or similar organization that offers physical activities or artistic or cultural activities, provided that the membership is for a minimum period of eight consecutive weeks in 2013 or in a subsequent year.

- Your family income does not exceed $130,000.

- You have a receipt that constitutes proof of payment of eligible expenses (registration or membership fees) for which you can claim the tax credit. You must keep your receipt in case we ask for it.

You or your spouse was not resident in Canada throughout the year

If you or your spouse was not resident in Canada throughout the year, you must take into account in calculating your family income all the income you and your spouse earned, including any income earned while you or your spouse was not resident in Canada.Calculating the tax credit

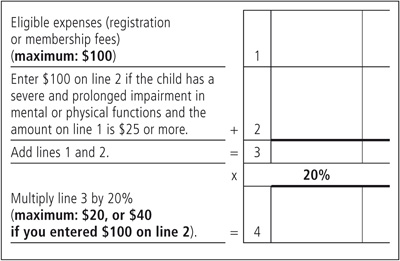

The tax credit is equal to 20% of the eligible expenses (registration or membership fees). The maximum amount of such expenses is $100 per child, for a maximum tax credit of $20 per child. If the child has a severe and prolonged impairment in mental or physical functions and the eligible expenses are $25 or more, you can add $100 to the amount of the expenses. Note, however, that the total of the two amounts (that is, $100 plus the amount of the eligible expenses) cannot exceed $200 per child, for a maximum tax credit of $40 per child.Use the work chart below to calculate the amount of the tax credit to which you are entitled. Calculate a separate amount for each eligible child and then add the amounts for all the eligible children together. Carry the total to line 462 of your income tax return.

Splitting the tax credit

If another person is also entitled to this tax credit for the same eligible child, the two of you can split the amount of the credit. While you can choose how to split the credit, the total amount claimed by both of you cannot exceed the amount to which you would have been entitled if only one of you were claiming the credit.Expenses that are not considered eligible expenses

You cannot claim the tax credit for any of the following expenses:- fees paid for a program of activities offered by a person who, at the time of payment, was either your spouse or under 18 years of age;

- fees for which anyone (you, your spouse or another person) received, or is entitled to receive, a reimbursement or any other form of assistance (with the exception of the non-refundable tax credit offered by the federal government), unless the reimbursement or assistance was included in that person's income and the reimbursement or assistance cannot be deducted elsewhere in that person's income tax return;

- fees that were used to calculate another deduction or refundable or non-refundable tax credit claimed by you, your spouse or another person.

- fees paid for an excellence in sport (Sport-Études) program.

Work chart

No comments:

Post a Comment